The use of IoT in commercial property to manage the total cost of risk (risk management and insurance spend) involves careful consideration of the commercial property’s unique risk profile, the particular perils they are exposed to, and the type of commercial buildings. The aim being to demonstrate a risk reduction and ideally risk avoidance by using IoT to manage the risk ‘better’ and thereby to open the conversation to more favourable premium terms and conditions with insurers.

IoT sensors provide a means to detect and respond to a range of hazards – some of which are insured, some will be within an insurance excess and some will be broadly risk avoidance through data-supported maintenance activity.

Based on 2020 data, global commercial property premiums totalled $140billion with price rises over 15 consecutive quarters. Globally, insurers paid claims of $88 billion.

The top causes of loss (perils) within commercial property are:

- Fire

- Escape of Water (inc Freeze)

- Theft

- All Others

IoT devices, real-time data and behavioural change can directly impact at least fire and escape of water incidents and theft. The focus being to reduce the $88billion in claims paid (which would be the values above any excess) as well as claims frequency more broadly and within any excess values.

A risk profile, the perils faced, and the nature of the commercial buildings, all play crucial roles in the IoT deployment strategy. By considering these perils based on the gross value of incurred claims (so those that are above the excess, below the excess or near misses), the ‘avoidance value’ of these perils can be used for the risk management/ insurance lens within a business case.

There are many IoT sensor options to monitor these risks such as power surge, smoke, and heat detectors for fire, water flow and temperature sensors for water incidents, and smart locks or intruder sensors for theft.

It’s worth noting here that whilst fire claims are the highest in value, they occur less frequently than water and theft incidents, which needs to be factored into any business case and subsequent prioritisation for IoT device deployment.

Aside from those three perils impacting the buildings themselves, there is also any stock to consider as well as any business interruption as a result of an incident. The ‘avoidance value’ for business interruption insurance cover is particularly interesting as IoT sensors align naturally with continuity of business operations (early warnings, early fixes etc).

When considering the application of IoT in commercial properties, the larger the commercial properties, typically the higher the premium values – meaning there is a greater potential impact on the total cost of risk by deploying sensors (and one of the many reasons why the ROI has not been there for residential property) and why risk is an essential component of any IoT business case.

Indeed, some insurers also offer risk management bursaries as part of their insurance offering to spend on risk management solutions such as ….. IoT !

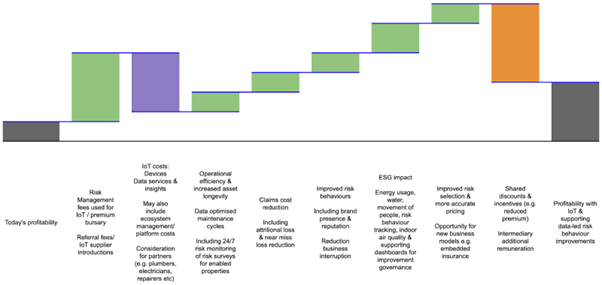

Sample business case impacts of IoT.

The deployment of IoT in commercial property must consider the risk and insurance lens when crafting a business case. A focus on the sensors to avoid and mitigate the highest frequency perils is a must and can be a significant determinant in the ROI calculation. With careful client selection and appropriate IoT technology, significant risk reduction and a more positive ROI can be achieved.

A former Head of Innovation & Emerging Technology at AXA XL’s IoT initiatives, Hélène Stanway is now the co-founder of the SENSE Consortium – a global forum driving the adoption of IoT and similar devices and the use of real time data to better manage commercial property risks in insurance. She consults and speaks globally to companies and insurance audiences about navigating and embracing digital innovation – helping them win with IoT and real time data technologies.